TL;DR

When a buyer panics after an inspection report, the agent’s job is to sort the findings into three buckets: safety concerns, maintenance items, and information only. The calmest path is to call the inspector, identify what actually needs action, then explain the findings in plain English before the buyer starts guessing.

- Safety concerns may need a specialist opinion, repair request, or stronger negotiation.

- Maintenance items usually need planning, pricing, or a credit conversation.

- Information-only findings give the buyer context without turning into a crisis.

The inspection report just landed. Your buyer called 7 minutes later. Their voice is tight. “There’s a lot wrong with this house. I don’t know if we should move forward.”

You open the web report. What they’re panicking about:

- Aging roof (18 years old)

- Water heater near end of serviceable life

- HVAC system showing wear

- Minor foundation cracks

- Moisture detected in attic

You know none of this kills the deal. But your buyer doesn’t know that. They just read 40 pages that sound like a disaster waiting to happen, and if nobody explains it in the next hour, they’re going to walk.

Here’s the thing: inspection reports aren’t written for understanding. They’re written for liability. The language is designed to protect the inspector from lawsuits, not to help your buyer make an informed decision.

“Water heater is near the end of its serviceable life” sounds terrifying when you don’t know that’s inspector-speak for “budget for a replacement sometime in the next few years.”

“Minor hairline cracks consistent with normal settling” sounds structural when you don’t know that every concrete foundation in Florida has these.

Your buyer doesn’t speak inspection. And if you don’t translate it for them, they’re going to Google it at midnight and convince themselves the house is in trouble.

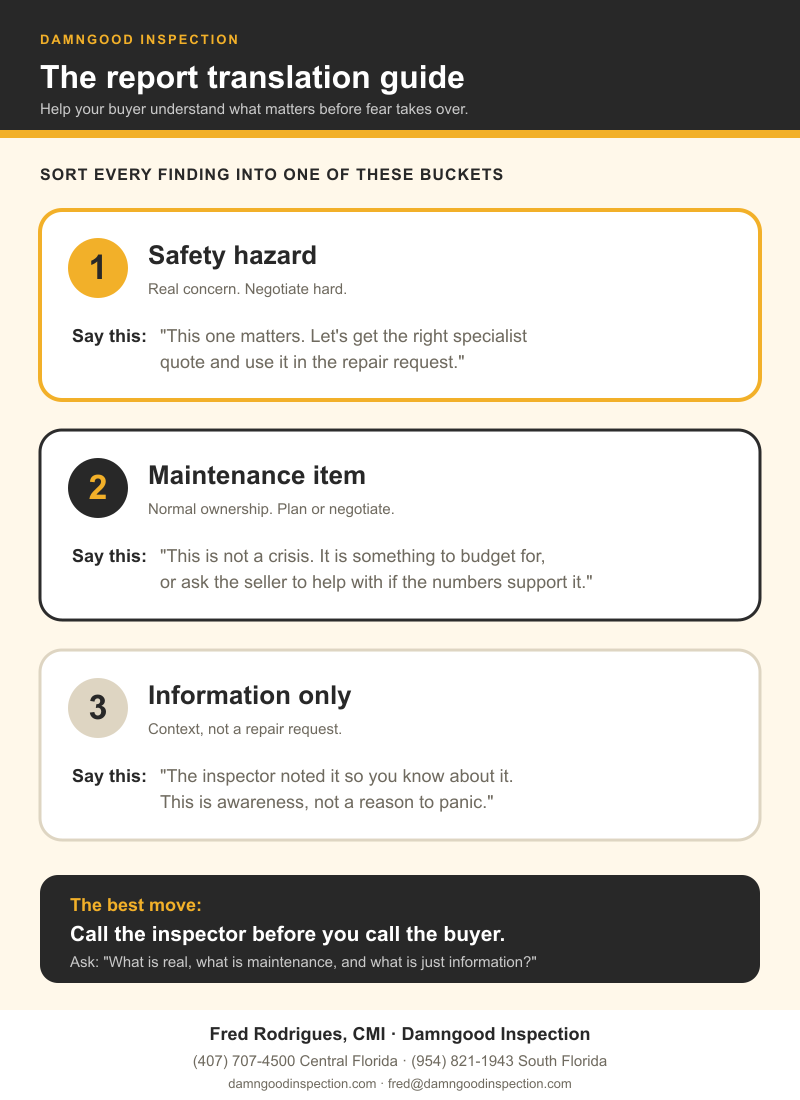

The Three-Category Framework

Before we get into the specific scripts, you need to understand how to sort findings. Everything in an inspection report falls into one of three buckets:

1. Safety Hazards (Negotiate Hard)

Electrical panels that are fire risks. Structural cracks in load-bearing walls. Active water intrusion. Polybutylene pipes that fail unexpectedly. These are real. This is your strongest negotiation leverage. When you bring these to the table, you’re protecting your client and they see you fighting for them.

2. Maintenance Items (Plan Ahead)

Water heater is 12 years old. Shingle roof is 15 years in and will need replacing soon. HVAC needs servicing. Every house has these. This is the bulk of every report, and it’s where buyers panic most often. When you explain “this is normal for a house this age, here’s how we handle it,” your buyer stops panicking and starts planning. That’s where you look like a pro.

3. Information Only (Context, Not Crisis)

Minor driveway cracks. Cosmetic wear on cabinet hardware. A scuff on the garage floor. Paint chipping on the fence. These aren’t repairs. They’re not problems. They’re just things the inspector wants your buyer to know exist. When you frame these as “FYI, not FYP (for your problem),” your buyer relaxes.

The agents who lose deals at inspection are treating all three categories the same. The agents who close are sorting them in real time during that phone call.

The 10 Most Common Florida Findings (And Exactly What to Say)

These scripts are word-for-word. Use them. Modify them for your voice. But don’t skip the pattern: acknowledge the concern, give context, tell them what happens next.

1. Aging Roof (15+ Years)

What your buyer hears: “The roof is failing. It’s going to leak any day. This house is a disaster.”

The reality: Shingle roofs in Florida typically last 15-20 years. After 15 years, insurance companies care. No active leaks means it’s still functional , it’s just aging.

What you say:

“The roof is 18 years old, which means it’s near the end of its expected life. The good news: no active leaks right now. The concern: some Florida insurance carriers may ask hard questions about older roofs, limit options, or price the policy differently. This is a real negotiation item. Here’s what we’re going to do: get a roofing estimate this week , probably $15,000 to $30,000 depending on the size , and we’ll ask the seller for either a credit at closing or a replacement before we close. That way you’re protected and you’re not surprised six months from now when your insurance carrier asks about it.”

Why it works: You separated “old” from “leaking,” gave them the insurance context, put a dollar amount on it, and told them exactly how you’re handling it.

2. Water Heater Age

What your buyer hears: “It’s going to fail tomorrow. I’ll have no hot water. It’s going to flood my house.”

The reality: Water heaters last 10-15 years. At year 12, it’s still working but near end of life. This is a planning item, not an emergency.

What you say:

“The water heater is 12 years old. Average lifespan is about 12-15 years, so it’s in the normal range. It’s working fine today , no leaks, no issues. This is a planning item. You’ll want to budget for a replacement in the next year or two. It’s about $1,200 installed for a standard 50-gallon tank. That’s normal homeownership, not a sign the house is in trouble. If you want, we can ask the seller for a small credit to offset it, but honestly, most sellers won’t budge on something that’s still working. Your call.”

Why it works: You gave them a timeline, a dollar amount, and normalized it as routine maintenance. Panic gone.

3. HVAC Age/Condition

What your buyer hears: “The AC is going to die. I’m going to be in Florida summer with no air conditioning.”

The reality: HVAC systems last 12-20 years depending on maintenance. Showing wear at 15 years is normal. If it’s cooling, it’s working.

What you say:

“The HVAC is 15 years old and showing some wear. It’s still cooling the house fine today, but at this age, you’re going to want to plan for a replacement in the next few years. In Florida, a good AC is essential, so this is something to be aware of. New system runs about $8,000 to $15,000 installed depending on the size of the house. This is a maintenance item , not a deal-breaker, but something to budget for. We can ask the seller for a credit if you want, or you can plan to replace it when it eventually goes. Your choice.”

Why it works: You acknowledged the concern, gave context on what “showing wear” actually means, and gave them control over how to handle it.

4. Electrical Panel Concerns

What your buyer hears: “Fire hazard. The house is going to burn down.”

The reality: Federal Pacific and Zinsco panels are known fire hazards. Modern breaker panels are fine. The inspector will note which kind it is.

What you say (if it’s Federal Pacific or Zinsco):

“The electrical panel is a Federal Pacific. These are known to have issues where the breakers don’t trip properly, which is a fire risk. Many insurance carriers do not like them, and some may require replacement before coverage. This is a safety item, so we’re taking it seriously. Let’s get an electrician out for a quote this week , probably $3,000 to $8,000 to replace the panel , and we’ll include it in our repair request. This is one reason inspections matter: they help buyers understand the real issues before they own the house.”

What you say (if it’s just old but functional):

“The electrical panel is outdated but working fine. It’s not a fire hazard, just old technology. This is more of an ‘eventually upgrade’ situation, not urgent. We can mention it in the repair request, but honestly, most sellers aren’t going to replace a working panel. Just know it’s there and plan for it down the road if you renovate.”

Why it works: You separated “real hazard” from “just old,” gave them action steps, and positioned it as your leverage.

5. Minor Foundation Cracks

What your buyer hears: “The foundation is failing. The house is sinking. This is structural.”

The reality: Concrete foundations in Florida crack. Humidity, heat, and settling cause hairline cracks. Structural cracks are wider, stepped, or horizontal. Inspectors note the difference.

What you say:

“Florida homes settle. The soil here shifts, concrete expands and contracts with heat and humidity, and minor hairline cracks are completely normal. The inspector noted these so you’re aware, but they’re cosmetic, not structural. If they were serious, the report would say ‘recommend structural engineer evaluation.’ It doesn’t. This is information, not a repair. You can seal them if you want , about $200 and an afternoon , but they’re not a problem.”

Why it works: You explained WHY it happens in Florida specifically, showed them how to tell the difference between FYI and crisis, and normalized it.

6. Moisture in Attic

What your buyer hears: “Mold. Water damage. The roof is leaking. This is going to cost me thousands.”

The reality: Attic moisture in Florida can be condensation, poor ventilation, or an actual leak. Inspectors note it to investigate further. It’s not always catastrophic.

What you say:

“The inspector detected moisture in the attic. In Florida, that can mean a few things: condensation from poor ventilation, a small roof leak, or just humidity. It’s not panic-worthy yet. Here’s what we’re going to do: get a roofer out to check for active leaks. If there’s a leak, we negotiate a repair. If it’s ventilation, that’s a smaller fix , adding vents or a fan, maybe $500 to $1,500. Either way, we’re not guessing. We’re getting a professional to pinpoint it and we’ll go from there.”

Why it works: You didn’t dismiss it, but you didn’t catastrophize it either. You laid out the possibilities and the plan.

7. Window Seal Failures

What your buyer hears: “All the windows are broken. I have to replace every window in the house.”

The reality: Dual-pane windows can fail where the seal breaks and moisture gets between the panes. It’s cosmetic (foggy glass), not functional. Annoying, not urgent.

What you say:

“Some of the windows have failed seals. That means there’s moisture between the glass panes, which makes them look foggy. It doesn’t affect insulation much, and the windows still open and close fine. It’s cosmetic. Replacing windows is expensive , about $300 to $800 per window , so most buyers just live with it unless it really bothers them. We can mention it in the repair request, but sellers almost never fix cosmetic stuff. Just know it’s there.”

Why it works: You set expectations on cost and how sellers typically respond. Your buyer isn’t blindsided.

8. Polybutylene or Galvanized Pipes

What your buyer hears: “The plumbing is going to fail. I’m going to have a flood.”

The reality: Polybutylene pipes (1978-1995) deteriorate from the inside and can fail unexpectedly. Galvanized steel pipes (pre-1960) corrode and reduce water pressure. Both are legitimate concerns.

What you say:

“The house has polybutylene pipes. These were used in the 1980s and 1990s, but they’re known to fail over time , they deteriorate from the inside and can fail unexpectedly. Insurance carriers often do not like them. This is one to take seriously. Repiping the whole house costs about $4,000 to $15,000 depending on size. This is a negotiation item. We’re going to ask the seller for either a credit or a repipe before closing. If they won’t budge, you need to decide if you’re willing to take that on. I wouldn’t sugarcoat it: this is a real expense.”

Why it works: You didn’t downplay a real safety issue. You gave them the facts, the cost, and the options. They trust you because you’re not just trying to close the deal at any cost.

9. Missing or Insufficient Hurricane Straps

What your buyer hears: “The roof is going to blow off in a storm.”

The reality: Hurricane straps (roof-to-wall connectors) are required by modern code but often missing in older homes. They’re important for wind resistance, and insurance companies care.

What you say:

“The inspector noted missing hurricane straps. These are metal connectors that tie the roof to the walls, and they’re important in Florida for wind resistance. Older homes didn’t always have them. Adding them costs about $1,500 to $3,000, and it’s something insurance companies look at when calculating your premium. We can ask the seller for a credit, or you can add them after closing. Either way, it’s a good investment for storm protection and insurance savings.”

Why it works: You explained what they are, why they matter in Florida, gave a cost, and made it manageable.

10. Termite/Pest Evidence

What your buyer hears: “The house is infested. It’s going to collapse.”

The reality: Florida is humid and wood-friendly for termites. Finding old evidence or active termites is common. It’s treatable.

What you say:

“The inspector found evidence of termite activity. In Florida, this is common , humidity and wood construction make it termite-friendly. The question is whether it’s old damage that was already treated, or active. We’re going to get a WDO inspection (Wood Destroying Organism) to confirm. If it’s active, treatment runs about $1,500 to $3,000, and we’ll ask the seller to handle it before closing. If it’s old damage, we’ll get a contractor to assess if any structural repairs are needed. Either way, we’re not closing until we know exactly what we’re dealing with.”

Why it works: You separated “evidence” from “active infestation,” gave them the process, and reassured them you’re not moving forward blindly.

The Call Before You Call Your Buyer

Here’s what top agents do that beginners skip: they call the inspector first.

Before you talk to your panicking buyer, you spend 5 minutes on the phone with the inspector and say:

“Walk me through the top 5 findings. What’s real, what’s maintenance, and what’s just information?”

Now when your buyer calls, you already know which findings matter and which ones don’t. You’re calm. You’re confident. You sound like someone who’s done this a thousand times. Because you have.

How to Use the Report as Negotiation Leverage (Not a Dead End)

Here’s the shift that changes everything: the inspection report isn’t a verdict. It’s ammunition.

Every finding is an opportunity to either:

- Negotiate a credit so your buyer gets money back at closing to handle it themselves

- Request a repair so the seller fixes it before closing

- Walk away if the seller won’t budge and the issue is too big

The agents who close deals after inspection are the ones who turn findings into negotiation points, not reasons to bail.

Example: “The roof is 18 years old and the HVAC is 15 years old. We’re asking for a $20,000 credit at closing to offset future replacements. If the seller says no, we’ll counter at $15,000. If they still say no, we decide if the house is worth it anyway.”

That’s control. That’s leverage. That’s how you keep deals together.

Save the report translation guide

If you want a simple way to talk through the report, use this three-bucket guide. It helps keep the conversation calm without downplaying real problems.

The Bottom Line

Your buyer isn’t scared of the findings. They’re scared of the unknown.

When you call them the same day the report lands, walk them through the findings category by category, give them context, and tell them what happens next , you’re not just saving one deal. You’re becoming the agent buyers trust.

They don’t remember the house had foundation cracks. They remember you explained it, calmed them down, and closed the deal anyway.

That’s the referral story they tell their friends.

FAQ

How long should I wait to call my buyer after the inspection report comes in?

Don’t wait. Call the same day, ideally within a few hours. The longer you wait, the more time your buyer has to Google findings and panic. If you call them first, you control the narrative.

Should I forward the full inspection report to my buyer, or summarize it for them?

Send the full report , they paid for it, they deserve to see it. But don’t just forward it and disappear. Call them and walk through the top findings before they read it alone. Context first, document second.

What if my buyer wants to walk because of minor findings I know aren’t a big deal?

Ask them: “Is this a deal-breaker because of the finding itself, or because you’re not sure what it means?” Most of the time, it’s fear, not facts. Walk them through the three categories (safety, maintenance, information) and show them what’s actually serious and what’s routine. If they still want to walk, respect it , but make sure it’s an informed decision, not a panicked one.

How do I know which findings to negotiate on and which to let go?

Negotiate on safety items (electrical hazards, structural issues, active leaks) and big-ticket maintenance that insurance companies care about (roof age, certain pipe types). Let go of cosmetic stuff and minor wear. You can’t fight every battle. Pick the ones that matter for safety, insurability, and resale value.

Should I recommend my buyer get a second opinion on major findings?

Yes, especially for electrical, structural, or plumbing concerns. If the inspector flags a Federal Pacific panel, get an electrician’s quote. If they note foundation cracks, get a structural engineer if you’re unsure. Second opinions give you negotiation ammunition and peace of mind. Just don’t use “second opinion” as code for “find an inspector who’ll say it’s fine” , that’s how deals blow up later.

What if the seller refuses to make any repairs or offer credits?

Then you and your buyer decide: is the house still worth it at this price, knowing what needs to be fixed? Sometimes it is. Sometimes it’s not. If your buyer loves the house and the issues are manageable, they might move forward anyway. If the seller is unreasonable and the findings are serious, walk. Don’t let your buyer inherit a disaster just to close a deal.

How do I explain the difference between a safety hazard and a maintenance item to my buyer?

Use this framing: “Safety hazards are things that could hurt you or cost you your insurance. We negotiate hard on these. Maintenance items are things every house has , stuff that’s aging but still working. We plan for these. Information items are just things the inspector wants you to know exist, but they’re not problems. We mostly ignore these.”

What’s the best way to handle a buyer who’s freaking out over an aging water heater or roof?

Normalize it. Say: “Every house built in the 1990s has an aging water heater. That’s not a red flag , that’s just how time works. It’s still working fine today. We’re just planning ahead.” Give them a dollar amount and a timeline so it feels manageable, not catastrophic.

Should I always call the inspector before talking to my buyer?

Not always, but on reports with major findings or anything you’re unsure about, yes. A 5-minute call to the inspector gives you clarity, context, and confidence. When your buyer calls panicking, you already know what matters. You sound like a pro because you did your homework.

How do I keep my buyer from Googling inspection findings at midnight and spiraling?

Call them first. If you explain the findings before they start Googling, they’re less likely to go down a rabbit hole. Also, literally tell them: “Don’t Google this stuff at 11 PM. It’s going to make it sound worse than it is. If you have questions after we talk, text me. I’d rather answer them than have you read horror stories on Reddit.”

Want an inspector who explains findings to your buyer in plain language so you’re not doing damage control?

That’s how we work. Call anytime.

Fred Rodrigues Damngood Inspection (407) 707-4500 (Central FL) | (954) 821-1943 (South FL) fred@damngoodinspection.com